What is a Credit Card Balance Transfer and Is It Worth It?

Are you struggling with credit card debt? A balance transfer might be the answer to your personal debt woes. If you’re paying credit card interest at 19.99 per cent or higher, it can take you a long time to pay off the outstanding balance. That’s where a balance transfer can help. If you’re disciplined and committed, you can save a lot of money with a balance transfer – just beware of the potential fees.

What is a Balance Transfer?

As the name suggests, a balance transfer allows you to transfer the outstanding balance owed to your current credit card issuer to another card at a lower interest rate. The point is to save money on interest payments. Although credit card interest rates are high compared to other types of consumer financing like personal loans and lines of credit, with a balance transfer you’ll often end up paying a lower interest rate.

Credit card issuers often try to lure cardholders with debt from rival issuers with low introductory rates. However, most issuers will not allow you to transfer a balance to another card from the same issuer.

What are the Advantages of a Balance Transfer?

A balance transfer can be an excellent way to save on interest. Balance transfers come with introductory rates as low as 0 per cent. If you have the cash flow to repay your outstanding balance, a lower interest rate means more money will go towards principal and less towards interest. Not only will you save on interest, you’ll pay off your balance a lot sooner.

A balance transfer can also make managing your finances a lot easier, especially if you have outstanding balances on more than one credit card. By transferring your balances to one issuer, you’ll only have one monthly payment to worry about. You’ll no longer have to worry about different interest rates and fees on different credit cards.

The Anatomy of a Credit Card Balance Transfer

The Anatomy of a Credit Card Balance Transfer

When Does the Regular Rate Kick In?

Before you sign up for a balance transfer, it’s important to find out when the regular, or “go-to” rate kicks in. The introductory period is different with every credit card, so review your cardholder agreement to find out. Introductory periods often range from as little as six months to 12 months or longer. The longer your introductory period, the better, as you’ll have more time to repay your outstanding debt at a reduced interest rate.

Before you start racking up new charges on your new credit card, it’s important to be aware that the lower interest rate almost always only applies to balances transferred from another credit card, not new purchases. You’ll still have to pay the regular interest rate on those purchases. Generally, making new purchases on your card is not advisable when trying to reduce debt levels.

Although a credit card may offer a low introductory rate of 0 per cent, if you only have six months to pay off your outstanding balance before a higher rate of 19.99 per cent kicks in, is it really worth it? Surprisingly, in many cases the answer is yes. It may be worth taking a slightly higher interest rate for a longer introductory period, especially if you have a lot of credit card debt. Use a credit card payoff calculator to help determine how much you can save.

Carrying a heavy debt load can affect your credit score. It’s important to read the fine print to make sure you qualify. Many balance transfers have minimum requirements for credit scores and earnings. Even if you don’t have a perfect credit score, it may still be worth applying. You could still qualify for a balance transfer, even if the introductory period isn’t as long.

Beware of Fees

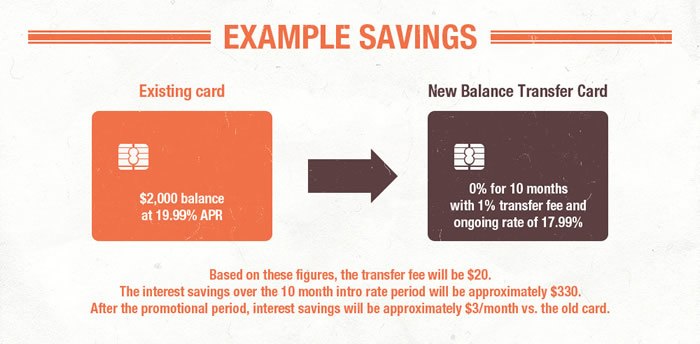

Before you sign up for a balance transfer, it’s important to find out about fees. A 0 per cent balance transfer may seem like a good deal, but is it really such a great deal if you have to pay a transfer fee of 3 per cent of your outstanding balance? Maybe…

Balance transfer fees usually range from 1 to 3 per cent of your outstanding balance. For example, if you’re transferring an outstanding balance of $5,000, you’ll pay a balance transfer fee of $50 at 1 per cent or $100 at 2 per cent. It’s important to do the math before signing up to see if it’s worth it. If you’re willing to repay your outstanding balance, despite the balance transfer fee, the interest savings from a low introductory interest rate is often worth it.

The Bottom Line

Balance transfers can be a great way to pay down your credit card debt. Shop around for introductory rates but be aware of any fees associated with the transfer. Make sure you understand the terms and conditions of any offer before applying, especially what happens when the into rate expires. Getting out of debt takes dedication, so put a solid plan together to get the most out of a balance transfer.