Good Debt vs. Bad Debt – The Key Differences between the Two Types of Debt

Posted in Debt, Personal Finance

Not all debt is bad. Sometimes carrying debt makes sense. With home prices hitting the stratosphere in many cities, it would take the average homeowner years to save up enough to pay for their home in cash. In fact, Millennials are struggling just to save the minimum five per cent down payment. Home prices have ballooned to 10 times the median income, over double the ratio in the 1980’s. In this case, taking on a mortgage makes sense.

While homeownership is often considered good debt, you want to avoid the opposite, bad debt. Bad debt usually means living beyond your means by constantly carrying a balance on your credit card. Let’s take a look at differences between the two types of debt and how you can stay clear of bad debt.

Good Debt

If you’re going to carry debt, ideally you want it to be good debt. Good debt is used to purchase assets – something that will provide a future benefit or grow in value. Examples of good debt include mortgages and student loans.

Although mortgages are considered good debt, homeowners can still find themselves in over their heads. If you purchase a home at the maximum purchase price approved by your bank, you could find yourself house poor, struggling to pay the mortgage and along with the carrying costs of your home.

Student loans are considered good debt because they are an investment for the future, as long as you’re able to land a well-paying job from your university degree. Although the income gap is narrowing, university graduates still earn significantly more over their career than individuals with only a high school diploma.

Good debt also helps build your net worth through the magic of leverage. Leveraging is when you borrow money to purchase an asset that increases in value. For example, if you purchase a home for $400,000 with a five per cent down payment ($20,000) and your home’s value increases by 10 per cent ($440,000), you’ve managed to double your equity to $40,000 – not bad!

Bad Debt

On the other end of the debt spectrum is bad debt. While good debt can help build your net worth, bad debt can hurt it. Bad debt is when you live beyond your means by borrowing money at high interest rates for stuff you don’t need or can’t afford. Examples of bad debt include car loans and borrowing money for vacations. Bad debt is often a substitute for saving – instead of putting aside $200 from each paycheque towards a family vacation, you simple charge it on your credit card and pay it off later.

(Some may view a car loan as good debt because the car is required for transportation to and from work. However, cars are depreciating assets. You’re better off buying a used car with saved cash and driving it into the ground.)

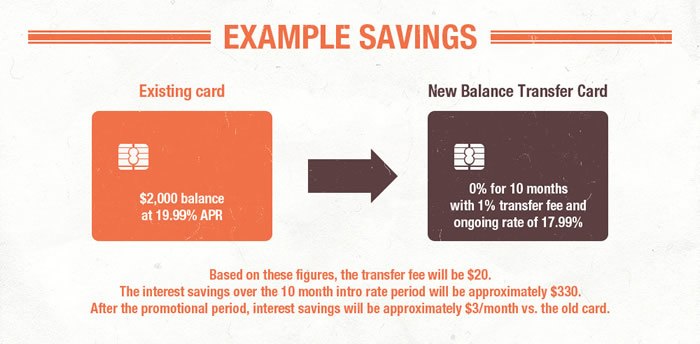

With bad debt, your purchases are generally consumed instantly or rapidly depreciate in value. Besides payday loans, the worst form of bad debt is credit card debt. Not only will it take you years to pay off your outstanding balance if you only make the minimum payment, it will likely cost you thousands in interest.

Your Credit Report

Before you’re approved for a mortgage or personal loan, the lender will often review your credit report. While reviewing your credit report, lenders will look at certain types of debt more favourably than others. If you’re maxed out on your credit cards, it will hurt your chances of being approved for further credit. You should carefully review your credit report and concentrate on paying off bad debt before good debt.

Concentrate on repaying revolving credit like credit cards, which typically carry the highest-interest rate, while you continue to pay the minimum on installment loans like your mortgage and student loan to keep them in good standing. In addition, you should aim to keep your credit utilization below 35 per cent of your available credit.

The Bottom Line

Good debt is debt used to buy assets that may increase in value over time – or that provide a means to grow wealth. Bad debt is using a credit card or loan to buy stuff you don’t need or can’t afford. Now that you have a better understanding of the differences between good and bad debt, you should take the time to review your outstanding debt. If you’re carrying a large balance on your credit card, you should concentrate on paying it down.